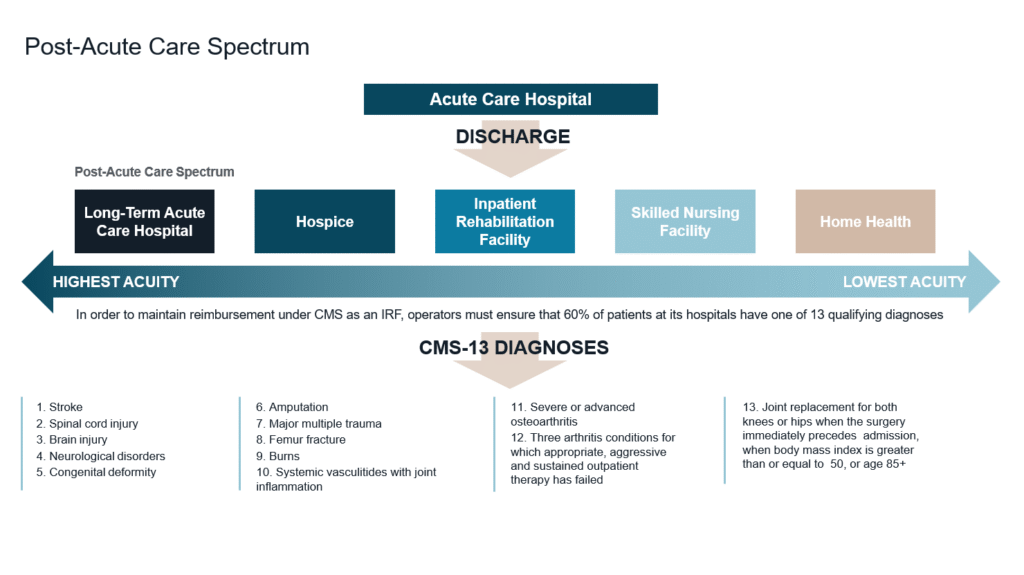

INPATIENT REHABILITATION HOSPITAL OVERVIEW

An inpatient rehabilitation hospital is a state-licensed acute-care facility dedicated to providing intensive rehabilitative services to patients recovering from major medical events such as strokes, orthopedic surgeries, neurological injuries, and complex illnesses. IRFs operate within the post-acute care continuum and serve patients who require daily physician oversight and multidisciplinary therapy following discharge from a short-term acute-care hospital. Compared to other post-acute settings, IRFs benefit from a relatively structured and predictable Medicare reimbursement framework, contributing to operational and revenue stability.¹

As investors seek durable yield in a decreasing interest rate environment, IRFs continue to attract interest from both domestic and foreign institutional capital—trends that show little sign of slowing. As capital markets normalize, IRFs have emerged as a rapidly expanding segment within U.S. healthcare real estate, benefiting from hospital-level care, long-term absolute net lease structures, durable demand fundamentals, and a development environment with high barriers to entry.

SUPPLY AND CONSTRUCTION TRENDS

As the ongoing shift from hospital-in-hospital rehabilitation units to freestanding inpatient rehabilitation facilities continues, the number of operating IRFs nationwide has increased from approximately 306 facilities in 2014 to more than 510 as of mid-2025—representing growth of roughly 67%.² This expansion has been driven primarily by freestanding IRFs developed in partnership with national operators, reflecting both rising demand for rehabilitation services and increasing institutional acceptance of the asset class.

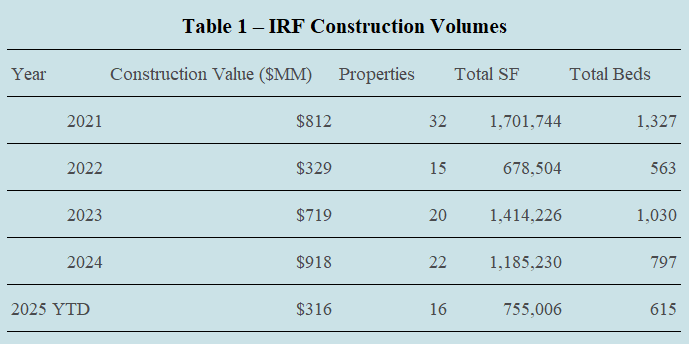

Consistent with this long-term growth trend, construction activity within the IRF sector has accelerated in 2025. According to RevistaMed, development volumes over the 12-month period leading into mid-2025 reached approximately 1.9 million square feet, surpassing the trailing twelve-month average of roughly 1.85 million square feet recorded from 2021 through 2024.² Table 1 outlines IRF construction activity from 2021 through year-to-date 2025.

Development volumes declined sharply in 2022 as rising borrowing costs, initial sticker shock around construction pricing, and a temporary misalignment between development yields and exit cap rates caused many projects to pause. Activity, however, quickly recalibrated as developers, institutional investors, and post-acute care operators recognized the recession-resilient nature of the IRF asset class, its essential role within the healthcare delivery continuum, and adjusted underwriting assumptions and deal terms accordingly.

From 2021 through the first half of 2025, more than 105 new IRF developments were delivered nationwide, totaling approximately 4,332 beds across 5.73 million square feet of new construction.³

IRF PRICING TRENDS

Freestanding IRF pricing for core-plus transactions in the United States has improved materially, with cap rates compressing from the high-6% to low-7% range during 2022–2024 into the mid-6% range in 2025.⁴ This improvement has been driven by increased equity capital entering the sector, tightening lender spreads and benchmark indices, and a steadily improving healthcare reimbursement environment.

GP EQUITY INVESTMENT THRESHOLDS IN IRF TRANSACTIONS

Equity structuring dynamics for IRFs have evolved as capital has become more experienced and selective. General partner equity contribution requirements for IRF acquisitions and developments have generally remained lower than those observed in non-healthcare asset classes, reflecting IRFs’ long-term lease structures, institutional tenancy, and recession-resistant cash flows. In most IRF transactions, GP investment thresholds typically range around 5-10% of total equity, allowing experienced operators and developers to remain economically aligned while still preserving sufficient sponsor diversification for equity partners.4

While equity investors in other commercial real estate sectors have pushed GP contribution requirements materially higher in recent years, IRF-focused investors have largely maintained more moderate thresholds. This has increased competition among sponsors and placed greater emphasis on differentiated operating strategies, health system relationships, and demonstrated execution capabilities within the IRF space.4

DEBT FINANCING AND LEVERAGE TRENDS FOR IRFS

Debt capital availability for IRFs remains robust but more conservative than during the prior low-rate cycle. In 2020 and early 2021, lenders were willing to advance highly levered financing for single-tenant healthcare assets; however, current IRF transactions are typically structured with loan-to-cost or loan-to-value ratios in the 60% to 65% range, depending on post-acute care operator scale, health system joint venture partner credit, lease term economics, and underlying market fundamentals.⁴

The reduction in leverage has widened the capital stack and created opportunities for common equity, preferred equity, and mezzanine capital to participate in IRF acquisitions and developments. For well-capitalized investors, this shift has improved risk-adjusted return profiles while reinforcing disciplined underwriting across the sector.⁴

2026 AND BEYOND

Looking ahead, IRFs are positioned to remain a key component of the U.S. healthcare ecosystem as the IRF healthcare delivery model aligns the interests of post-acute care operators, patients, and governmental payors, creating a framework that supports quality outcomes, operational efficiency, and reimbursement sustainability. These attributes make IRFs an attractive asset class for institutional capital, a trend we expect to continue for the foreseeable future.

REFERENCES

¹ Centers for Medicare & Medicaid Services (CMS), Inpatient Rehabilitation Facility Overview.

2 RevistaMed, “Rehabilitation Hospital Construction Showing Signs of Rising in 2025.”

3 RevistaMed, Post-Acute and Rehabilitation Hospital Real Estate Data, 2021–YTD 2025.

⁴ Colliers US Healthcare Capital Markets Research.