As health systems face growing pressure to optimize capital and accelerate growth, many are turning to third-party developers and property owners to support their real estate needs. Using Revista’s inventory of medical outpatient buildings (MOB) larger than 7,500 square feet, we examined which health systems are leading this shift and how third-party development and ownership are shaping healthcare real estate strategies.

Ownership trends reveal that health systems still occupy a substantial amount of owner-controlled space, while REIT- and investor-owned outpatient buildings affiliated with health systems account for approximately 352 million square feet nationwide, highlighting the growing role of third-party ownership in healthcare real estate. Leading the way in both third-party ownership and development, the Veteran’s Health Administration (VHA) occupies ~14.9 million square feet of REIT- and investor-owned outpatient space, followed by HCA Healthcare at ~10.5 million square feet. Regional systems such as Piedmont Healthcare and Baylor Scott & White stand out because investor-owned properties account for more than 60% of their occupied space. Even among systems with significant leased portfolios, ownership remains dominant. For example, Kaiser Permanente occupies roughly 5 million square feet in investor-owned properties but maintains an owner-occupied portfolio of nearly 29 million square feet.

On the development side, health systems continue to overwhelmingly favor self-development, supported by strong hospital acquisition activity and ongoing investment in owner-controlled real estate. However, third-party development remains an important component of the healthcare real estate landscape, particularly for organizations seeking greater flexibility, faster project delivery, or reduced capital exposure. Since 2021, the VHA has led all health systems with 55 third-party developed MOB projects totaling approximately 4.3 million square feet, followed by HCA Healthcare with 24 projects and roughly 1.1 million square feet.

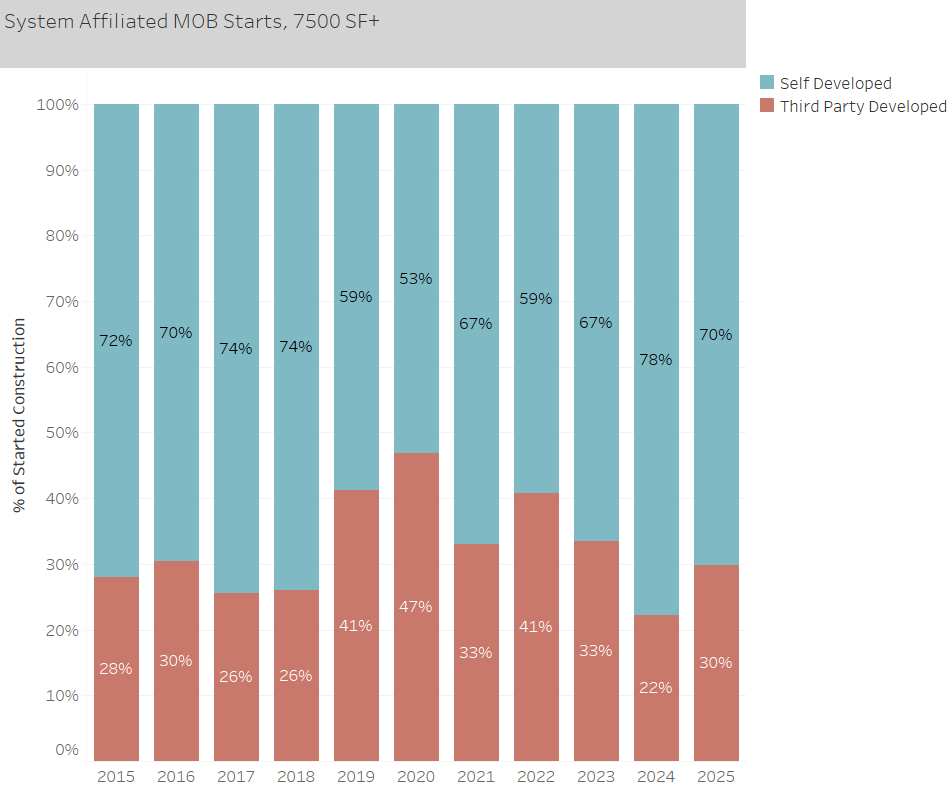

Although third-party MOB development starts declined to 22% in 2024, activity rebounded to 30% in 2025, while third-party developed completions have steadily increased over the past five years. This trend suggests that even as health systems continue to prioritize ownership and self-development, external developers still play a meaningful role in helping systems expand outpatient networks and bring projects online efficiently.

Rather than signaling a retreat from ownership, the data points to a more strategic allocation of capital. As health systems balance rising operational costs, technology investments, and ambulatory growth initiatives, third-party owners and developers provide an avenue to expand while preserving capital, mitigating development risk, and accelerating speed to market.