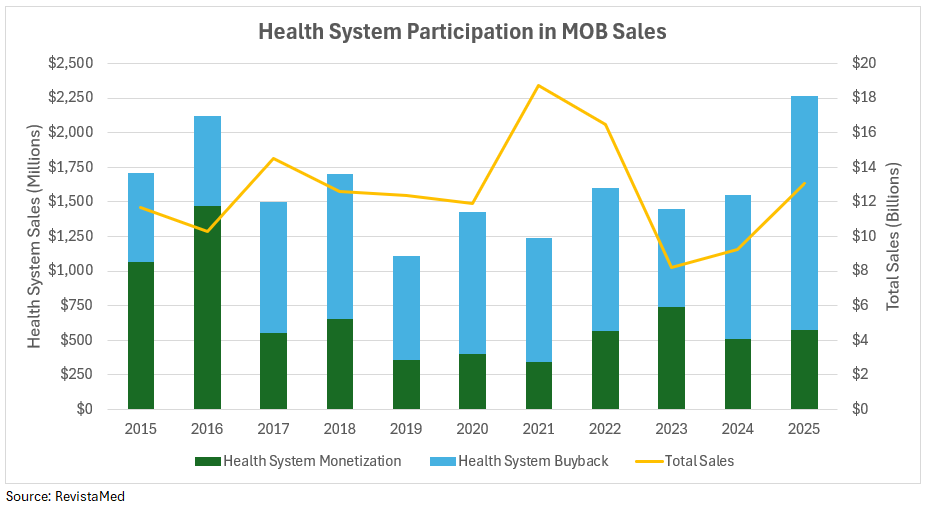

Health systems have been one of the most active participants in the medical properties investment sales market in the last 3 years, accounting for 17% of all sales activity as either the buyer or seller. In 2025 alone, health systems bought $1.7 billion of their leased properties – a record year – making up 13% of all sales. According to RevistaMed, this buyback phenomenon is comprised of 82 individual properties acquired by 58 systems. Nearly half of the buyback volume – 45% – was owned by the 3 largest public REIT owners of outpatient medical. While a good portion of the sales to health systems were triggered by planned dispositions with tenant rights of first refusal to purchase, many health system acquisitions were negotiated on a non-contractual basis.

Why are health systems buying back leased properties at a time of heightened concern about operating margins and adverse impact from the Big Beautiful Bill?

- Outpatient buildings are more essential than ever. The high growth in outpatient services and the increasing acuity of services in ambulatory settings has resulted in more buildings considered core to operations and fully occupied by health systems. The compounded growth rate in ambulatory care in the last 10 years is high at 6%. More surgical procedures, diagnostics, imaging and invasive treatments occur in outpatient settings. Health systems today derive the majority of their revenue from outpatient care. Particularly at major health centers with more intensive infrastructure, health systems have a preference to own and control the real estate.

- There are higher levels of liquidity at not-for-profit health systems today, resulting in high days cash on hand (DCOH), a key metric to fortify bond ratings. Median DCOH tracked by the major rating agencies was 230 days prior to COVID. DCOH in 2025 returned to this same level, largely due to record levels of equity investment values driving the absolute value of health system cash and investments. The rate of increase in operating expenses is outstripped by the accelerated value of cash and investments in today’s market, thereby increasing DCOH.

- Strong access to the municipal bond market with favorable tax-exempt rates today, typically 100 basis points lower than taxable rates. While long-term borrowing rates have risen dramatically since Q1 2022, A and AA-rated not-for-profit health systems can borrow close to 4.0% on a tax-exempt basis.

- Growing awareness and use of alternative lease financing for health systems. Lease financing through credit tenant leases and synthetic leases has been used by health systems for buybacks and build-to-suit projects. While the volume of these financings is dwarfed by bond issuance, it offers attractive financing for outpatient medical at health systems’ cost of taxable or tax-exempt debt, in addition to bond financing.

Prepared by: Mindy Berman, mindy.berman66@icloud.com +1 617 899 0657